Key Takeaways

- Invoice financing in Singapore allows SMEs to unlock cash tied up in unpaid customer invoices, improving immediate cash flow management without taking on new debt.

- There are two main types: Invoice Factoring (selling the invoice) and Invoice Discounting (borrowing against the invoice).

- Unlike traditional business loans, approval is based primarily on your customers’ creditworthiness, not just your own company’s financial history, making invoice financing for small businesses accessible even without long trading histories.

Picture this: You’ve wrapped up a major project for a client, but when the invoice goes out, you spot in the payment terms: “Net 60”. That’s a two-month wait before you see a single dollar.

In Singapore, it’s business as usual for many SMEs to sell on credit. Your client pays in 30, 60, or even 90 days. But your overheads aren’t kind enough to wait: rent, salaries, supplier payments, and new inventory costs all pile up, risking a cash flow crunch that can choke growth or force you to delay new orders.

This is where invoice financing steps in—not as a traditional loan, but as a strategic tool that converts your unpaid invoices into immediate working capital.

In this comprehensive guide, we’ll break down the mechanics, types, process, and key considerations of online invoice financing, so you can decide if it’s the right fit for your SME.

What is Invoice Financing?

Definitions and Key Concepts

At its core, invoice financing is a funding method where a business sells its outstanding invoices (accounts receivable) to a third‑party financier—commonly called a “factor”—in exchange for immediate cash.

Instead of waiting for your customer to pay according to the credit terms, you receive an advance that typically ranges from 70% to 90% of the invoice value within 24 to 48 hours. The remaining balance, minus a service fee, is released once your customer settles the invoice.

Key Differentiators Between Invoice Financing and Business Loans

Invoice financing is not a loan in the conventional sense:

- There’s no new debt sitting on your books

- You’re simply unlocking the value of an asset you already own—the invoice.

The cost of this invoice financing comes in the form of a discount fee or factor fee, usually a percentage of the invoice value calculated per week or per month until the customer pays up.

Another key differentiator from traditional business loans is that approval is based primarily on your customers’ creditworthiness, not just your company’s own financial history. This makes purchase invoice financing and other forms of receivables‑backed funding especially attractive for younger SMEs or those with modest balance sheets.

Recourse vs. Non‑Recourse Factoring

Recourse: If the customer fails to pay, your business must buy back the invoice or cover the loss. This is more common—and cheaper—because the factor (the third‑party financier) does not assume the credit risk.

Non‑Recourse: The factor assumes the risk of customer non‑payment (credit risk). Fees are higher, and the factor will conduct strict credit checks on your customer beforehand. This option provides protection against bad debts.

Two Types of Invoice Financing for Businesses to Consider

Many SME owners aren’t aware that there are actually two distinct forms of invoice financing. The right type of Singapore invoice financing solution for you depends on (i) how much control you want to keep and (ii) how much of the collection process you’re willing to outsource.

Invoice Factoring

Invoice factoring involves selling your invoices to a factoring company (a.k.a. the factor), which then advances a percentage of the invoice value and takes over the collection process. You get cash quickly, and the factor chases payment on your behalf.

Do note the critical distinction when it comes to customer awareness:

- Notification Factoring: Your customer is informed that a third‑party financier is involved and that the customer pays the factor directly. This is the standard arrangement for most factoring in Singapore.

- Confidential Factoring: The factor handles collection under your business name, so the arrangement stays private. Less common and more expensive due to the extra administrative work involved.

Factoring often includes a complete credit control service, freeing up your team from chasing payments. In Singapore, notification factoring is the more prevalent model, particularly for SMEs who prefer to outsource the hassle of debt collection.

Invoice Discounting

Invoice discounting is a more discreet cousin of factoring. Here, your unpaid invoices serve as collateral for a line of credit or a short‑term loan. You retain full control of your sales ledger and continue managing the debt collections yourself. Your customers typically never know a financier is involved; they pay you as usual, and you then settle the advance with the financier.

The key advantage is confidentiality. Because the relationship with your customer remains untouched, discounting suits larger, more established companies that already have a strong internal credit control team. It’s also popular among businesses that worry that using a factor might create the wrong impression for their clients.

In Singapore, discounting is usually reserved for companies with a proven track record of managing receivables efficiently.

The Mechanics of Invoice Financing

Cash Flow Management and Its Importance

Cash flow is the lifeblood of any SME. A business can be profitable on paper yet still grind to a halt if money isn’t flowing in right when it’s needed. That’s why robust cash flow management isn’t just a task for the finance team—it’s a strategic priority.

Fumble your cash flow management, and you might miss out on growth opportunities. For instance, you might have to turn down a large, profitable order simply because you can’t afford the raw materials upfront while waiting 60 days for other invoices to clear.

For many SMEs, invoice financing is a powerful working capital solution that shortens your cash conversion cycle (the period between paying your own suppliers and receiving payment from your customers).

Businesses in need of additional working capital could also explore our working capital loan options, which offer flexible, unsecured funding for a range of operational needs.

How is Accounts Receivable Financing Structured?

Let’s walk through a typical purchase invoice financing arrangement using a tangible example that reflects the industry’s shift toward digital verification and transparent fee modelling:

- Invoice Value: S$100,000 (sold to a creditworthy corporate customer).

- Advance Rate (typically 80%): S$80,000 is transferred to your corporate bank account within 24–48 hours of invoice verification.

- Customer Pays (60 days later): The full S$100,000 is remitted to the financier (in a notified factoring setup) or to your business (in discounting).

- Settlement: The financier deducts the S$80,000 advance and their fee. Suppose the factor fee is 3% of the invoice value = S$3,000.

- Remaining Balance (Rebate): S$100,000 – S$80,000 – S$3,000 = S$17,000 is returned to your business.

The fee structure often works on a time‑based calculation: for example, 1% per 30 days on the amount advanced. Some business invoice financing providers charge a flat percentage per invoice, while others levy a monthly interest rate on the outstanding amount.

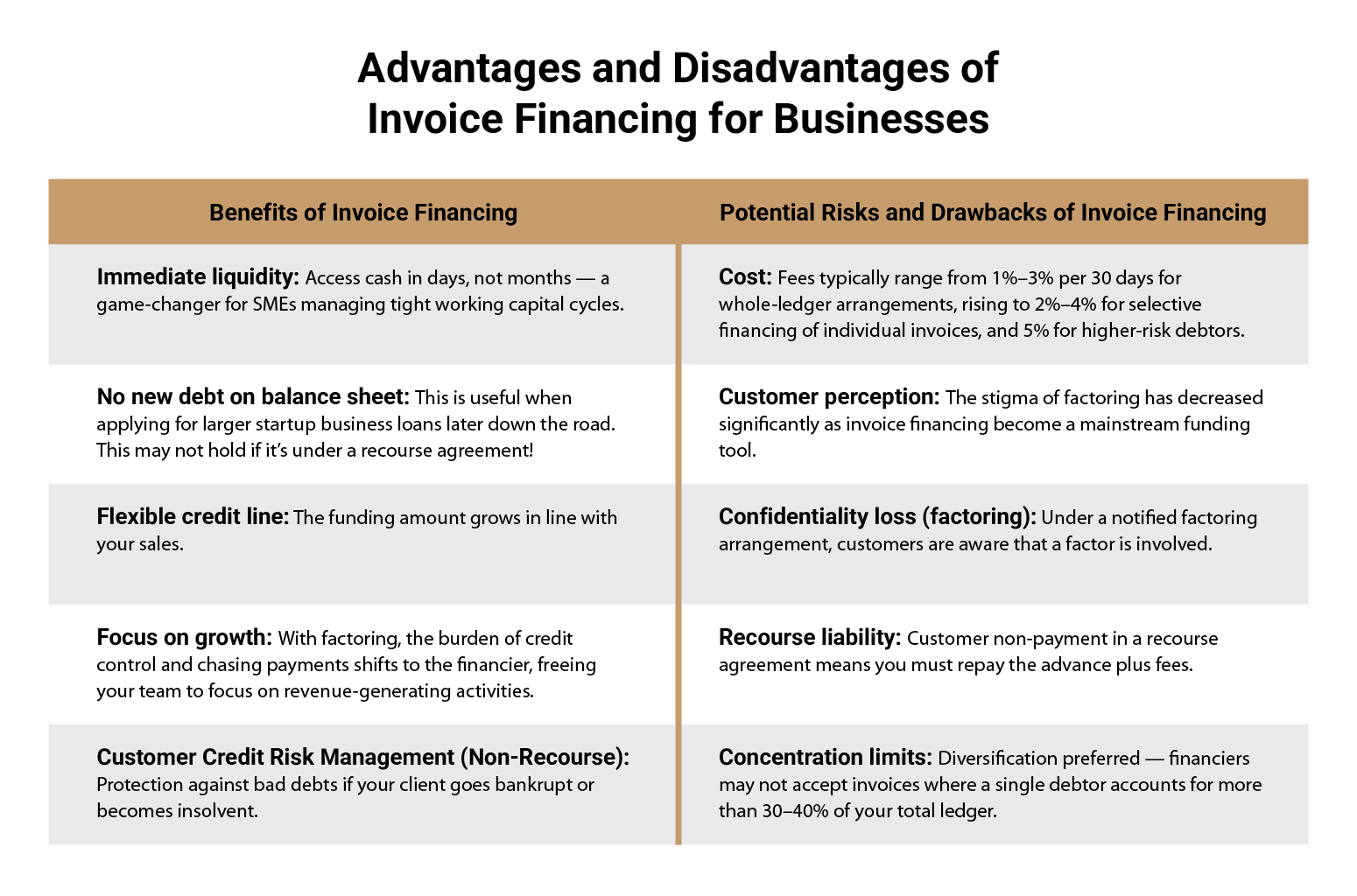

Advantages and Disadvantages of Invoice Financing for Businesses

Benefits of Invoice Financing

Immediate liquidity: Access cash in days, not months — a game‑changer for SMEs managing tight working capital cycles.

No new debt on balance sheet: This is useful when applying for larger startup business loans later down the road. This may not hold if it’s under a recourse agreement!

Flexible credit line: The funding amount grows in line with your sales.

Focus on growth: With factoring, the burden of credit control and chasing payments shifts to the financier, freeing your team to focus on revenue‑generating activities.

Customer Credit Risk Management (Non‑Recourse): Protection against bad debts if your client goes bankrupt or becomes insolvent.

Potential Risks and Drawbacks of Invoice Financing

Cost: Fees typically range from 1%–3% per 30 days for whole-ledger arrangements, rising to 2%–4% for selective financing of individual invoices, and 5% for higher-risk debtors.

Customer perception: The stigma of factoring has decreased significantly as invoice financing become a mainstream funding tool.

Confidentiality loss (factoring): Under a notified factoring arrangement, customers are aware that a factor is involved.

Recourse liability: Customer non-payment in a recourse agreement means you must repay the advance plus fees.

Concentration limits: Diversification preferred — financiers may not accept invoices where a single debtor accounts for more than 30–40% of your total ledger.

Should I Choose Invoice Financing in Singapore for My Business?

Before deciding, ask yourself these questions:

Do you have slow‑paying customers? If you regularly wait 45–90 days for payment, invoice financing for small businesses can smooth out your cash flow.

Is your business model seasonal? For example, a catering company might have incredibly busy festive seasons but then face a long wait for receivables. Export invoice financing can be particularly useful for traders who deal with cross‑border clients.

How close are your client relationships? Would your key clients object to a third party managing collections? If confidentiality is paramount, consider invoice discounting instead.

What resources do you have? If you lack a dedicated credit control team, factoring might be the smarter, less stressful route.

What else could you do with the freed‑up cash? Sometimes, the return from investing early‑received funds (e.g., taking on a large project or bulk purchasing at a discount) far outweighs the cost of financing.

If, after weighing these factors, you’re still exploring other funding solutions, take a look at our best SME loans in Singapore page or consider a business expansion loan for long‑term growth initiatives.

FAQ

Startups may also benefit from our guide on startup business loans. For asset purchases, check out our guide to hire purchase. Each solution has its own eligibility criteria and a dedicated account manager to support you along the way. Speak to us or simply submit your online application anytime you’re ready!